For high-net-worth investors holding assets in Dubai, property insurance has shifted from a compliance requirement to a core pillar of asset management. This is not a minor adjustment; it is a fundamental recalculation of risk, driven by severe weather events that have reset market perceptions. Entering 2026, comprehensive coverage is an essential mechanism for safeguarding capital appreciation and ensuring rental yield continuity.

The New Risk Calculus for Dubai Property Investors

The market has matured from the post-Covid boom into a sustainable growth cycle. The record transaction volumes of last year have now stabilized, demanding a more analytical approach from investors. This shift is most apparent in how risk, specifically asset insurance, is now approached.

For years, property insurance was treated as a formality to satisfy a mortgage requirement. That conversation has fundamentally changed. Proactive risk mitigation is now central to portfolio management, and a robust insurance policy is its cornerstone. This is not about covering minor damages; it is about protecting a portfolio against systemic shocks that can erode long-term asset value.

Climate Events Reshaping The Insurance Sector

The April 2024 floods were a definitive turning point. The storm triggered unprecedented insurance payouts and sent UAE gross written premiums soaring by 14.5% to AED 40.9 billion in H1 2025. This event was the catalyst for the widespread adoption of specific flood riders, pushing average premiums up by nearly 20% over the following year.

This single event forced insurers and property owners to re-evaluate vulnerabilities, especially in low-lying or coastal communities. A risk once considered almost negligible is now a primary factor in every premium calculation.

For HNWI investors, the implications are direct, particularly for those holding waterfront villas in emerging master communities like Palm Jebel Ali or luxury penthouses with extensive terraces. Insurers now scrutinize building specifications, drainage infrastructure, and elevation data with a level of detail previously unseen.

From Compliance to Strategic Asset Management

This new market reality demands a proactive stance. Accepting a standard, off-the-shelf policy is no longer adequate for a high-value portfolio.

- Portfolio Review: The first step is to audit existing policies to identify coverage gaps, looking specifically for clauses related to floods, storms, and water damage.

- Yield Protection: Landlord policies that include loss of rental income are no longer optional. Extended repair times can impact cash flow, and this coverage ensures continuity.

- Capital Appreciation Shield: A major uninsured event can diminish a property's market value. Comprehensive insurance acts as a shield, guaranteeing the asset can be fully restored, thereby protecting its capital appreciation trajectory.

The current dynamics reflect a maturing market where protecting assets is as critical as acquiring them. Understanding this shift is essential, as our comprehensive Dubai real estate market analysis indicates that well-managed, securely insured properties will command a premium. In 2026, the discussion is not if you need comprehensive property insurance in Dubai, but how you structure it to align with your portfolio's long-term financial goals.

Deconstructing Coverage for Your Dubai Real Estate Portfolio

Managing a high-value real estate portfolio in Dubai requires viewing property insurance not as a single product, but as a layered defense. Each layer is designed to neutralize a specific financial threat. Understanding how these layers work together is key to building a resilient asset.

The core of a robust insurance strategy is built on three pillars: Building Insurance, Contents Insurance, and—the most critical for investors—Landlord Insurance. Each plays a distinct role. Missing one can leave a significant exposure in your financial armor.

Building Insurance: The Foundational Layer

This is the armor for the asset itself. Building insurance covers the physical structure of your property—walls, roof, windows, and permanent fixtures—against catastrophic events like fire, explosions, or natural disasters. For villa owners, this is non-negotiable; securing this policy is your direct responsibility.

If you own an apartment, this coverage is typically managed by the building’s owners' association and bundled into annual service charges. Do not assume it is adequate. Verifying the details of this master policy is critical. An underinsured building can lead to massive, unexpected levies on all owners after a major incident.

Contents Insurance: Protecting Interior Assets

This policy protects all movable items inside your property, including furniture, high-end appliances, electronics, and personal belongings. While often considered for owner-occupiers, it is vital for investors offering premium, turnkey rental units.

A fully furnished luxury apartment in Downtown or a branded residence derives its value from its high-spec fit-out. If that interior is damaged, the property becomes un-rentable, and you face a significant bill to return it to an income-generating state. This policy ring-fences that internal investment.

Landlord Insurance: Securing Your Yield

This is the most crucial—and most frequently overlooked—policy for a property investor. Landlord insurance is engineered specifically to protect your rental income stream. It looks beyond the physical asset to shield the financial performance of your investment.

Its key protections are designed to maintain cash flow consistency.

- Loss of Rental Income: If your property becomes uninhabitable after a fire or major flood, this policy pays you the lost rent during the repair period.

- Tenant Default: Select policies offer protection if a tenant stops paying rent, providing a crucial financial buffer.

- Public Liability: This covers legal costs if a tenant or visitor is injured on your property, a critical protection.

For an investor, yield consistency is paramount. Landlord insurance acts as a financial stabilizer, converting the unpredictable risk of damage-induced vacancy into a fixed, manageable operational cost.

Understanding the nuances between ownership types is also key. The insurance obligations for freehold vs leasehold properties can vary, especially regarding responsibility.

To clarify, I've broken down how these three core policies fit into an investor's strategy.

Core Insurance Policies for Dubai Property Investors

This table outlines the essential insurance products, their coverage, and their strategic importance from an investment perspective.

| Policy Type | Primary Coverage Scope | Strategic Importance for an Investor |

|---|---|---|

| Building Insurance | Covers the physical structure of the property (walls, roof, fixtures) against catastrophic events like fire, floods, and storms. | Essential for villas; for apartments, it protects against shortfalls in the building's master policy, preventing large, unexpected repair levies. |

| Contents Insurance | Protects all movable items inside the unit, from high-end furniture and appliances to art and electronics. | Critical for investors offering furnished, turnkey units. It safeguards the "product" being rented and ensures rapid replacement to minimise downtime. |

| Landlord Insurance | Covers loss of rental income due to property damage, tenant default (optional), and public liability claims from tenants or visitors. | Directly protects cash flow and ROI. It is the only policy that specifically secures the investment's financial yield, not just its physical value. |

These policies are not interchangeable. They work in concert to create a comprehensive shield that protects not just the brick-and-mortar asset, but the income it generates.

What Drives Your Insurance Premium?

Calculating the cost of property insurance in Dubai is a direct function of risk. For an investor, understanding this equation is key to trimming the operational costs of a real estate portfolio. Insurers evaluate every property through a specific lens, weighing factors that influence the likelihood and potential cost of a claim.

Core factors include property value, location, age, and construction quality. A new branded residence in a prime, inland location will receive a better premium than an older villa on the waterfront, now perceived as having a higher flood risk. This perception has shifted dramatically since last year's storms, making location a more important factor.

To manage your premium, it helps to understand how various insurance quote request forms function. Knowing the information they require lets you present your asset in the best possible light.

Quantifying The Variables

An insurer's calculation reflects the perceived risk. For a high-value property, these elements are scrutinized:

- Location & Environmental Risk: A penthouse in Downtown has a different risk profile than a ground-floor villa in Palm Jebel Ali. Proximity to water, elevation, and community infrastructure quality are now top-tier data points.

- Property Valuation: The higher the declared value of the building and its contents, the higher the base premium. Accurate valuation is critical. Underinsuring can lead to a catastrophic loss; overinsuring wastes money on inflated operational costs.

- Construction & Age: Newer properties built to the latest codes almost always secure better rates. The quality of materials, from fire-retardant cladding to modern electrical systems, directly lowers risk in the insurer's view.

- Occupancy Type: Whether the property is owner-occupied, rented long-term, or used as a holiday home changes the premium. Short-term lets often cost more due to higher footfall.

Smart Moves to Lower Your Premiums

The best way to manage insurance costs is to actively reduce your asset's risk profile. Insurers are data-driven; they reward verifiable safety upgrades with direct premium reductions. This is where you can take control.

A common myth is that insurance premiums are fixed. The reality is they are negotiable figures based on provable risk. Investing in specific safety technology protects your asset and actively lowers its running costs. This is a core principle of smart asset management.

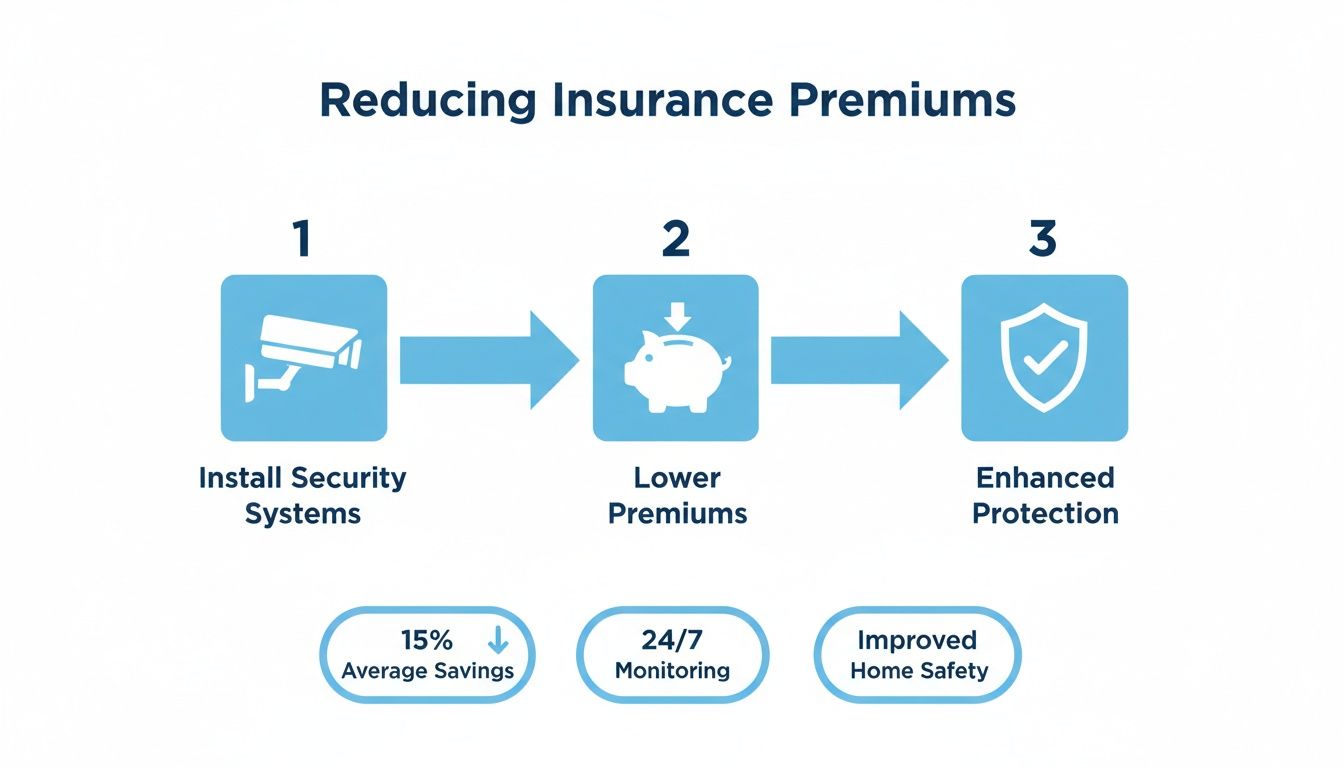

Data from last year shows that installing certified security and safety systems can reduce premiums by 15-20%. Across a property portfolio, those savings become material.

Actionable Steps to Reduce Your Premium:

| Mitigation Strategy | Description | Potential Premium Impact |

|---|---|---|

| Advanced Security | Installing RERA-compliant, centrally monitored CCTV, alarm systems, and smart locks. | High (10-15% reduction) |

| Fire Suppression | Upgrading to modern smoke detectors, installing sprinkler systems, and using fire-retardant materials. | High (10-12% reduction) |

| Water Damage Prevention | Installing automated water shut-off valves, leak detectors, and for villas, flood barriers. | Moderate to High (5-10%) |

Even with these upgrades, the Dubai property market forecast shows that the underlying value of well-protected assets continues to climb, making these small investments a high-ROI decision.

Looking at 2025 benchmarks, property insurance in Dubai remains cost-effective. Annual premiums for villas were often just AED 800 to AED 1,500—a fraction of the cost in other global property hubs. Key drivers were location and security measures, and investors with multiple properties secured portfolio discounts of 10-25%. This reinforces Dubai’s value proposition for international HNWIs.

Navigating The Claims Process for Swift Recovery

An insurance policy is only as good as its ability to pay out quickly. For an asset manager, swift financial recovery is everything. The claims process in Dubai has become remarkably efficient, but understanding its mechanics is key to minimizing property downtime and protecting rental yield.

The entire process hinges on meticulous, immediate documentation. Delays in reporting or patchy evidence are the primary reasons claims get bogged down. The first action after ensuring safety must be to contact your insurer and broker.

The Initial Steps Are Critical

From the moment an incident occurs, you are building your case for a settlement. The first 24-48 hours are the most important for gathering the proof your insurer will demand.

- Immediate Notification: Do not wait. Call your insurance provider immediately. Most policies have a strict timeframe for reporting a claim; missing it creates an unnecessary complication.

- Evidence Collection: Photograph and video everything from every angle before anything is moved, cleaned, or repaired. For theft or vandalism, a police report is non-negotiable and will be one of the first documents requested.

- Damage Mitigation: You have a responsibility to take reasonable steps to prevent further damage, such as turning off a water main after a leak. Document these actions.

To get paid efficiently, you must understand the technical proof your insurer expects during a claim in Dubai. This includes not just photos but detailed contractor invoices and expert assessments for structural issues.

The Power of Technology in Claims Processing

Dubai's insurance sector has invested heavily in technology, changing the process for property investors. What was once complex and opaque is now more transparent and efficient.

AI-driven claims processing has reduced settlement times from a standard 14 days down to under 5 days. This is not just about convenience; it builds investor confidence by demonstrating a modern, responsive ecosystem that protects assets effectively.

This infographic shows how proactive measures, like installing modern security systems, not only reduce risk but can also directly lower your premiums.

Insurers reward landlords who actively mitigate risk.

Documentation Checklist for Common Claims

Organized paperwork is half the battle. This documentation is also vital for managing the details within the tenancy contract Dubai requires, especially concerning the property's condition before and after an incident.

For high-value or complex claims, appointing an independent loss assessor is a strategic move. They work on your behalf, not the insurer's, to accurately quantify the loss and ensure your interests are fully represented during settlement negotiations.

For Water Damage:

- Dated photos and videos of the initial damage and its source.

- A plumber's report detailing the cause of the leak.

- Invoices for all repair and restoration work.

For Fire Damage:

- The official report from Dubai Civil Defence.

- A complete inventory of every damaged item with its estimated value.

- Quotes and final invoices for all structural repairs and content replacement.

A well-documented, promptly filed claim is the final step in ensuring your property insurance in Dubai delivers on its purpose: protecting your capital and cash flow.

A Due Diligence Checklist For Selecting An Insurer

Choosing the right insurer in Dubai is as critical as selecting the right property. This decision goes beyond a simple premium comparison. You are vetting a long-term financial partner whose performance will directly impact your portfolio's stability.

The lowest premium is often a false economy, potentially leading to an insurer with a poor claims payment track record. A sophisticated investor looks past the price to an insurer's financial health and operational efficiency—the metrics that matter when protecting a high-value asset.

Analyzing Financial Stability

Before reviewing a policy, assess the insurer's financial strength. A policy's value depends on the provider's ability to pay large claims, especially after a city-wide event like the 2024 floods.

Look for their credit rating from agencies like AM Best or S&P Global Ratings. A strong rating, typically 'A-' or higher, signals a stable financial position. This is a non-negotiable, third-party validation of their long-term viability.

Scrutinizing Claims Settlement Ratios

The claims settlement ratio is a direct measure of an insurer's real-world performance. This annual figure shows the percentage of claims paid against the total received.

A consistently high claims settlement ratio—ideally above 90%—is a powerful indicator of a customer-focused approach and an efficient process. A low ratio is a major red flag.

This is a data point we track at Proact. It separates reliable providers from those likely to create friction during a critical recovery phase.

Expertise in High-Value Real Estate

Not all insurers are equal. A provider focused on basic auto or home insurance may lack the underwriting sophistication for luxury properties. You need an insurer who understands the specific risks of high-end finishes, smart home technology, or valuable collections.

Their policy wording should reflect this expertise. Look for clear sub-limits and extensions for high-value items, not generic clauses. This is vital when assets are held within a corporate structure, as the policy must align with the standards of a proper Dubai LLC company setup.

Here’s what to focus on:

- Policy Exclusions: Pay close attention to what is not covered. Common exclusions include damage from faulty workmanship or gradual wear and tear.

- Sub-Limits: Check the maximum payout for specific categories like electronics or jewelry to ensure it aligns with the actual value.

- Broker Relationships: Working with a brokerage with strong relationships with A-rated insurers can provide access to better terms and a smoother claims process.

Final Thoughts: Strategy Over Compliance

In Dubai's sophisticated market, treating property insurance as an administrative task is a significant error. The mindset of assuming basic cover is "good enough" or that a major event is unlikely is a direct path to financial exposure. That era is over.

Today's market demands a strategic view. Your insurance policy is not just a compliance document for the bank; it is a core component of your asset's financial architecture, built to protect both capital and rental yield. Proactive risk management, through a properly structured insurance plan, is the only way to safeguard your return on investment.

From Annual Expense to Portfolio Shield

Thinking of your insurance premium as just a yearly expense is an outdated perspective. Reframe it as an investment in your portfolio's stability and resilience. A robust policy shields your cash flow from the effects of an unexpected interruption.

This strategic mindset separates passive property owners from serious asset managers who understand that long-term value is built on a foundation of managed risk. The right coverage protects against tomorrow's challenges, whether from evolving climate patterns or shifting market dynamics. It provides the confidence to operate, knowing your portfolio is built to withstand shocks.

As you plan and rebalance your Dubai real estate portfolio for 2026, a strategic review of your insurance coverage is non-negotiable. At Proact Luxury Real Estate, we integrate this critical analysis into every client's strategy.

Frequently Asked Questions

When protecting high-value property in Dubai, details matter. Investors often have practical questions about how insurance works. Here are the most common queries we handle.

Is Property Insurance Mandatory In Dubai For Homeowners?

While not legally mandatory for all owners, it is a practical and often contractual necessity. If you have a mortgage, your lender will insist on building insurance as a non-negotiable condition of the loan.

For villa owners, arranging building insurance is fundamental asset management. For apartment owners, the building's master policy is covered in service charges, but this creates a critical gap. That policy does nothing for your interiors, belongings, or rental income. Operating without your own contents and landlord insurance is an unacceptable risk.

How Does Insuring An Off-Plan Property Differ?

Insuring an off-plan property involves protecting it through different phases of risk. During construction, the developer is legally required to have a Contractor's All-Risk (CAR) policy. This covers the structure while being built, and RERA’s escrow rules protect your financial payments.

The moment of handover is the critical switch. The second you take possession, the developer’s responsibility ends, and liability for insuring the asset becomes yours. Your own building insurance (for villas), contents, and landlord policies must be active at this point to ensure no coverage gaps.

Does Standard Property Insurance Cover Loss Of Rental Income?

No, a standard building or contents policy is designed to pay for the cost of repairing or replacing physical items. It offers no compensation for lost rent while the property is uninhabitable during repairs.

Protecting your cash flow is the specific job of a Landlord Insurance policy. This specialized cover is engineered to pay out for lost rent after an insured event, like a major fire or flood. If your investment strategy is built on rental yields, this policy is indispensable.

Can I Get A Discount For Insuring Multiple Properties?

Yes, portfolio discounts are a standard feature in Dubai's insurance market. Top A-rated insurers offer multi-property discounts when you consolidate all policies with them.

For HNWIs and family offices, these reductions can be material, typically ranging from 10% to 25% off the total premium. Beyond cost savings, it simplifies administration with a single point of contact for all claims and renewals. Consolidating your asset base can also simplify other processes, like securing a golden visa UAE.

At Proact Luxury Real Estate, we believe that protecting your assets is as important as acquiring them. If you are rebalancing your portfolio for 2026, let's run the numbers and ensure your insurance strategy is as robust as your investment.